How SECURE Act 2.0 Affects You

January 17, 2023

How to Pick a Health Plan

March 15, 2023

Many of us place a high value on frugality and simplicity. Byzantine emperor Justinian I said, “Frugality is the mother of all virtues.” English writer Samuel Johnson said, “Without frugality none can be rich, and with it very few would be poor.” We are safer and smarter if we part with our dollars thoughtfully.

This explains in part why I think most Americans do not work with a financial advisor. I read a report* from December 2022 that showed the biggest barrier to working with a financial professional is “perceived cost of advice.” Of course, I thought. If you don’t know what you’ll get, how can you possibly perceive the value?

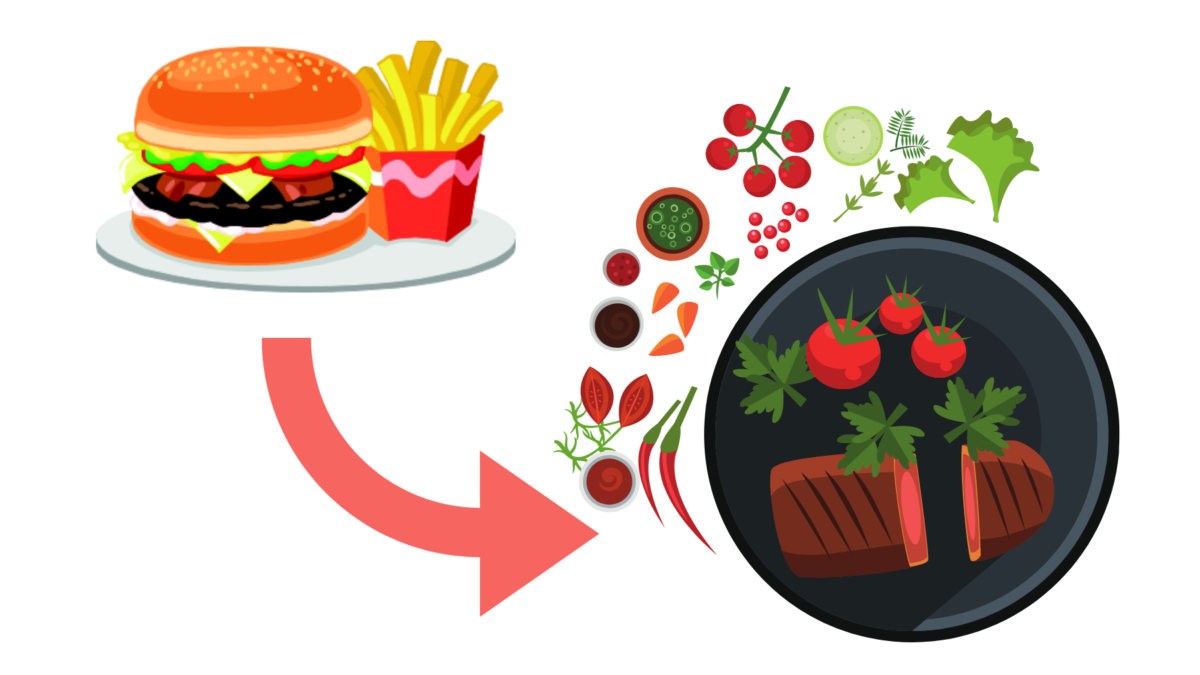

Advice on investments—that is mostly what most people expect a financial advisor to bring to the table. This can be thought of as a burger and fries. The burger is managing investments. The fries? Maybe they’ll get guidance about how much to save, how to get out of debt or how to manage risk through insurance.

No wonder then that the perceived value falls short of the cost. Many people have figured out the basic rules about investing are not complicated. Diversify across types of assets and manage expenses, turnover, and taxes. The simplest way to do this is to buy well-diversified, inexpensive indexed mutual funds and exchange-traded funds.

You read that and you might think, “I know investing doesn’t have to be complicated. Why do I need to pay someone to do what I can do myself?” Let’s break it down and along the way I can make my point about the value of working with someone like me.

Here’s the hard part about investing: stay disciplined through market dips and swings. The reason to not have all your eggs in one basket—diversify—is that in the long run you have more money. But it means that when the market is up your investments don’t go up as much as the top performing asset class, and when the market is down your investments still go down, just not as low as the lowest performing asset class. It looks like either way you lose. Our human nature craves gratification and so this isn’t all that satisfying. We’re not wired to look at the long run.

As far as managing costs, what should be the obvious ones—avoiding mutual funds with high investment expense ratios and transactions costs—are the mistakes I see the most. It is not unusual to see annual fund expenses around 1% and financial planning fees around 1%, which eat into your return—with significant long terms costs because returns are what you eat. If you know how to look for these, and don’t work with a financial advisor who recommends them, this can be accomplished.

More complicated is making tax-aware investment decisions. This includes what types of assets to hold by type of account (brokerage, tax-deferred or tax-free), because the tax treatment preferences certain investments over others. Other decisions with tax implications are where you invest your Income Portfolio to fund your lifestyle after fulltime work, rebalancing, and gifting to family and charity.

Now let’s say you’ve read the above and realize you need to lower your investment costs or diversify. Doing this in a tax-smart way makes a big difference. Then there’s the value that comes from shifting assets from tax-deferred to tax-free accounts with a Roth conversion, which will benefit you by reducing your tax burden later when taxes are likely to be higher and reducing the tax burden for your heirs. Options such as charitable giving through your IRA if you’re over 70 ½ or gifting highly appreciated assets to a Donor Advised Fund, just two examples, are also worth considering.

In addition to these services, financial advice can help you with choices everyone has to make. Here are a couple: understanding when the optimal timing is to start Social Security and evaluating options for healthcare coverage and Medicare at pivotal moments such as getting married, changing jobs, moving, and retiring. These can provide tangible value from increased benefits or lower costs.

Financial advice can help with decision paralysis, which results in the common mistake of keeping most of your money in cash or not spending when you could be flourishing instead of surviving. Helping you prepare for changes down the road—such as what you would want if you couldn’t live independently or manage your affairs—avoids burdening a loved one with those decisions amidst chaos and crisis.

Finally, a mistake I see comes from the best of intentions and results in nothing but trouble: people think that diversifying across accounts and institutions (instead of types of assets) will protect them from financial ruin. What it does is create paperwork complexity in your lifetime and a huge headache for your heirs. Every institution has its own forms and rules, and these will have to be navigated not once or twice but over and over when it comes to settling your estate.

Now that we’ve added a medley of roasted vegetables to our plate and trimmed the fat off that burger, we can look at the value of being guided through a structured exploration of your values and goals, and having a financial plan that aligns with what’s at your heart’s core. Here is the special sauce that ties the plate together: financial freedom from stress and worry because you know how much you can spend, what you’re invested in and why, the “What If” scenarios around aging or economics that will require adjustments, and that you have an “Exit Continuity Plan” to make it easier for your loved ones to carry on when you’re not here.

*Edelman Financial Engines December Report, “Everyday Wealth in America 2022 Report”